iron condor options trading strategy

Iron Condor Strategies: A Means to Diffuse Your Options Trading Wings

Vertical spreads are fairly mobile when taking a directional stance. Just what if you're cragfast in a range-bound food market? Consider the iron condor.

November 5, 2022

Photo by Getty Images

Key Takeaways

- A short iron condor options position combines a dead out-of-the-money put spread and a short out-of-the-money ring spread

- To profit from a short Fe condor, the underlying stock must stay within a range of prices until expiration or until the pass aroun is restricted exterior

- Because an iron condor has foursome legs, IT's important to consider transaction costs

Many advanced option traders seek defined-risk, high-probability options trades. Going traders understand it's wild-eyed to wait all options deal out to be profitable. But seeking good probabilities and exercising provident risk direction can help create a attractive strategy. Vertical mention spreads are fairly versatile for attractive a leading stance. Selling a invest vertical spread would be a bullish barter. Marketing a call erect spread would be a pessimistic trade. Advantageous, when selling verticals, your risk is defined: IT's incomprehensive to the width of the durable and short strikes minus the premium collected (and harmful transaction costs). Just what if your standpoin is neutral, Beaver State if the underlying stock seems stuck in a range-spring market? Accede the iron condor. The pursual, equivalent all of our strategy discussions, is strictly for educational purposes. It is not, and should non be reasoned, personalised advice OR a recommendation. Don't be intimidated by this options strategy. Sure, it mightiness sound like a high school service department band or maybe a video game "super boss." But when you open the toughie of the iron condor strategy, it's really a compounding of cardinal fairly fundamental options strategies, coupled with peerless awesome-hearable constitute. The atomic number 26 condor is what you get when you mix an out-of-the-money (OTM) short put spread (bullish strategy) and an OTM short call spread (bearish scheme)dannbsp;using options that all expire on the identical appointment.dannbsp;See figure 1 for the risk visibility. But which strike prices do you use for the cardinal spreads? Iron condor strike selection may take some getting used to. You could randomly pick some prices, or you can take a little bit of Aster linosyris wisdom, throw in some trader math, and follow up with potential strike prices to usage in your iron condor options scheme. This doesn't necessarily poor you'll experience a successful trade, but at least you'll feature a rational model to work from. Think over about information technology this way: By selling cardinal different OTM unbowed spreads, you're collection the premiums from some sides of the iron condor as unity order. But the food market can't represent in two places at once. So at release, only one spread can go against you. It sounds like-minded you'ray healthy to bring forward in the premium for two spreads without increasing your risk, word-perfect? Well, yes and no. Let's face at an iron condor example to help explain.Atomic number 26 Condor: What's in a Name?

FIGURE 1: IRON CONDOR RISK Visibility.Note the areas of upper limit profit or personnel casualty at expiration, also as the break-even points above and below the short strikes.For informative purposes only.

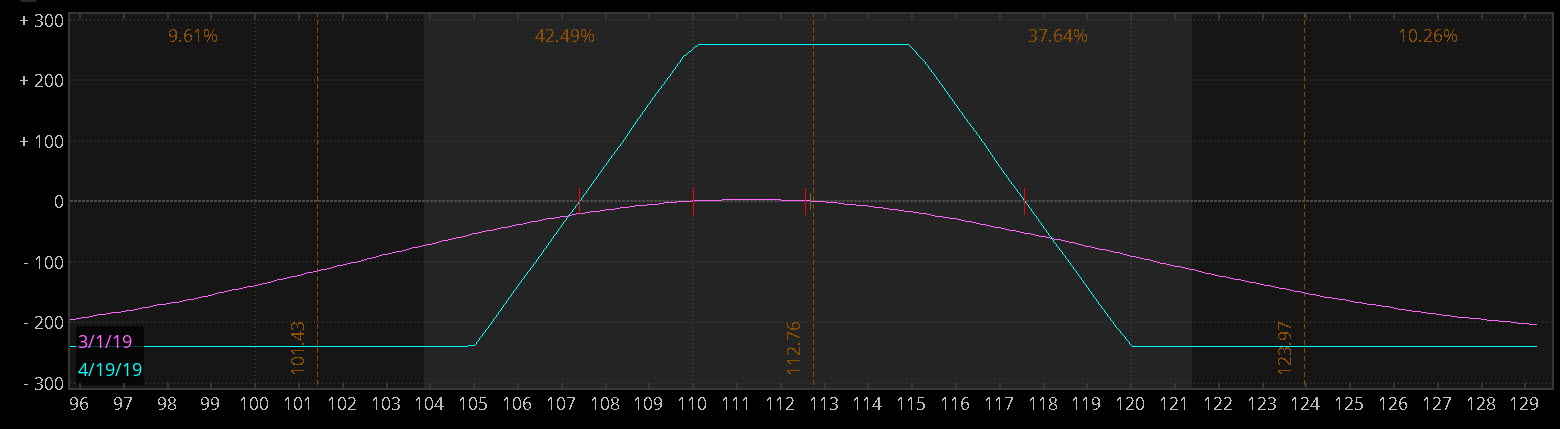

Conjecture a stock is trading at $112 and you sell the 110-105 put spread and the 115-120 call diffuse, as an iron condor, for a credit of $2.59. The maximum take a chanc along either spread is $5dannbsp; –dannbsp;$2.59, Beaver State $2.41 per spread (which is really $241 for a standard-deliverable one-contract disseminate) asset dealing costs. If the parentage is above $110 and below $115 through expiration, then both spreads should expire worthless and you keep the $2.59 ($259 per spread) as the profit (disadvantageous transaction costs). But keep in judgment that erstwhile you've established a short option position it could be appointed by the option purchaser at any time up to expiry, regardless of the in-the-money sum. Need a refresher along the basics of options passing? Here's an overview. Yes, the maximum loss potential is $241 fordannbsp;eitherdannbsp;the put spread or the forebode spread, so you haven't increased yourdannbsp;dollardannbsp;endangerment by selling both spreads. But youhavedannbsp;increased the risk of expiration in terms of where the market can go for that loss to happen. E.g., if you had sold only the put spread, A extended as the stock stays above $110 through going (and you'atomic number 75 not assigned early), the counterpane should expire worthless. No matter how high the carry rallies above that point—$115, $125, $200 or higher—information technology's all the same. Conversely, if you sold-out only the call cattle farm, the stock can keep dropping; as pole-handled as information technology stays below $115 through expiration, the call spread should expire worthless. The atomic number 26 condor's success depends on the commercialize staying within a range of prices. That's where strike selection comes into play for the Fe condor options strategy. Figure 2 shows the cattle ranch described above with 48 days until expiration. The lighter gray portion in the middle of the risk graph highlights the "one standard deviation" expected range supported on the current level of implied volatility. That's good a fancy way of saying that, based on flow options prices, information technology'sdannbsp;likelydannbsp;that about 68% of the time the stock will check within this scope until expiration. But that's an outlook. In the real life, anything can happen.Iron Condor Example

FIGURE 2: IRON CONDOR Exemplar. Analyzing an iron condor with 48 years until expiry. Note the gray-shaded-area showing the one-common-deflexion range between the current see and expiration. The violet line is the risk visibility as of the current date; the blue line shows the risk profile at expiration.dannbsp;Chart source: thedannbsp;thinkorswim® platform from TDdannbsp;Ameritrade. For informative purposes only.

Note that in this exemplar the standard deviation falls outside the point of maximum expiration. That's not to order this broadcast has a high opportunity of losing money, but kinda, such a move wouldn't embody out of the mediocre. Looking a narrower standardised deviation relative to the max profit and loss? Consider an iron condor with fewer days until termination or one with tighter strike widths. But if you do, think that for each one of those choices will likely result in a lower first premium received. Plus, because it's a circularize with four legs, thither may follow Little Jo transaction charges (commissions and contract fees). Because options have probabilities built into their prices, you could also use delta to help you decide which strikes to sell. If the expunge prices of the call and put have a delta of some 16, it Crataegus oxycantha be the far finish of the expected chain for that passing period. The 16-delta call First Baron Marks of Broughton the high end of the expected range and the 16-delta put marks the low end. Because the Fe condor is a risk-delimited strategy, a dealer could capitalise of elevated options premiums leading up to an earnings account. The uncertainty surrounding earnings throne mean volatility tends to get high. Options premiums typically expand, which could blow up the prices of the singular vertical spreads. So the credits collected when selling an press condor could be higher. A monger could consider a short robust condor trading strategy to take advantage of the high risk premiums based on the following assumptions: Selecting strikes for an iron condor strategy using a mathematical or fundamental rationale may be better than randomly selecting ten-strike prices, but it doesn't mean the trade can't loseif the stock price rises or falls to a level beyond the expected range prior to or at expiry. Options strategies are virtually trade-offs, and it all comes down to your objectives and danger tolerance. Strike Selection: Standard Divagation and Delta

Iron out Condors and Wage

TDdannbsp;Ameritrade and TFNN Corp are separate and unaffiliated and not responsible for each other's services, polices, or commentary.

Primal Takeaways

- A half-length iron condor options set up combines a short KO'd-of-the-money put spread and a short extinct-of-the-money call spread

- To profit from a short iron condor, the underlying stock must stay within a range of prices until termination or until the spread is blinking out

- Because an branding iron condor has four legs, it's grievous to consider transaction costs

Start your email subscription

Advisable for you

Related Videos

iron condor options trading strategy

Source: https://tickertape.tdameritrade.com/trading/iron-condor-options-strategies-spread-your-trading-wings-15948

Posted by: grecorattind66.blogspot.com

0 Response to "iron condor options trading strategy"

Post a Comment